4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025)

Imagine a future where you're no longer chained to a desk, trading your precious time for a paycheck. Early retirement sounds idyllic, doesn't it? But how do you ensure your nest egg lasts the distance? This is where the 4% Rule comes in, a guiding principle for calculating a safe withdrawal rate. Let's dive into the updated 2025 version and see how it can help you achieve financial freedom.

The allure of early retirement often bumps against the harsh realities of financial planning. Concerns about outliving your savings, unexpected expenses, and the ever-present specter of inflation can quickly dampen the enthusiasm. Navigating the complexities of investment portfolios and market fluctuations can feel overwhelming, especially when the stakes are so high.

This guide aims to demystify the 4% Rule, offering a clear understanding of its principles, its limitations, and how it can be used as a tool for planning a comfortable and sustainable early retirement. We'll explore its history, dissect its assumptions, and provide practical advice for adapting it to your individual circumstances. The target is to provide our readers with knowledge about 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

In essence, the 4% Rule is a guideline to help you determine how much you can safely withdraw from your retirement savings each year without running out of money. We'll examine its historical context, discuss potential pitfalls, and offer strategies for customizing it to your specific needs and risk tolerance. Key terms you'll encounter include safe withdrawal rate, early retirement planning, investment portfolios, inflation, and financial independence. Stay tuned as we unlock the secrets to a secure and fulfilling retirement!

My Personal Journey with the 4% Rule

I remember when I first stumbled upon the 4% Rule. It was during a particularly stressful period in my career, where the thought of escaping the rat race consumed my every waking moment. The idea of retiring early seemed like a distant fantasy, a luxury reserved for the ultra-wealthy. Then, I read about this seemingly simple rule that suggested a path to financial independence was within reach. The initial excitement quickly turned to skepticism. Could it really be that straightforward? Was it too good to be true? I spent countless hours researching, poring over articles, and running simulations. The more I learned, the more nuanced the picture became. The 4% Rule wasn't a magic bullet, but rather a framework for making informed decisions. It highlighted the importance of understanding my own risk tolerance, the intricacies of investment portfolios, and the potential impact of inflation. Today, as I refine my own early retirement plans, the 4% Rule remains a valuable tool, constantly being adapted and adjusted based on my evolving circumstances and the latest market data. It's not about blindly following a number, but about understanding the underlying principles and using them to create a personalized roadmap to financial freedom. The concept of safe withdrawal rate and investment portfolio performance are very important keywords that are related to 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025). The initial excitement quickly turned to skepticism. Could it really be that straightforward? Was it too good to be true? I spent countless hours researching, poring over articles, and running simulations.

What Exactly is the 4% Rule?

At its core, the 4% Rule is a guideline for determining a sustainable withdrawal rate from your retirement savings. It suggests that you can withdraw 4% of your initial portfolio value in the first year of retirement, and then adjust that amount annually for inflation, without significantly increasing your risk of running out of money over a 30-year retirement period. This rule is based on historical stock market data and inflation rates, primarily from the United States, and aims to provide a reasonable balance between living comfortably in retirement and preserving your capital for the long term. The beauty of the 4% Rule lies in its simplicity. It offers a tangible starting point for retirement planning, allowing individuals to estimate the size of the nest egg needed to support their desired lifestyle. However, it's crucial to understand that the 4% Rule is not a one-size-fits-all solution. It's a historical guideline that may not accurately reflect future market conditions or individual circumstances. Factors such as life expectancy, investment allocation, and spending habits can all significantly impact the success of the rule. The key is to use it as a foundation for your retirement planning, adjusting it based on your own unique situation and continually monitoring your progress. Understanding inflation and spending habits is the key to adjusting 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025). The beauty of the 4% Rule lies in its simplicity. It offers a tangible starting point for retirement planning, allowing individuals to estimate the size of the nest egg needed to support their desired lifestyle.

The History and Myth of the 4% Rule

The 4% Rule wasn't plucked out of thin air. It emerged from extensive research conducted by financial advisor William Bengen in the 1990s. Bengen analyzed historical stock market data and inflation rates from the past century to determine a safe withdrawal rate that would have allowed retirees to maintain their standard of living for at least 30 years. His research, originally focused on a portfolio consisting of 50% stocks and 50% bonds, found that a 4% withdrawal rate had a high probability of success across various historical periods. However, it's important to dispel some common myths surrounding the 4% Rule. Firstly, it's not a guarantee. Historical data doesn't predict the future, and unexpected market downturns or high inflation could jeopardize its effectiveness. Secondly, it's not necessarily theoptimalwithdrawal rate. Some retirees may be able to withdraw more, while others may need to withdraw less, depending on their individual circumstances and risk tolerance. Finally, the 4% Rule isn't set in stone. It's a guideline that can be adjusted based on changing market conditions and personal needs. Understanding the historical context and the limitations of the 4% Rule is crucial for making informed retirement planning decisions. William Bengen did extensive research to help analyze historical stock market data and inflation rates from the past century to determine a safe withdrawal rate that would have allowed retirees to maintain their standard of living for at least 30 years. This information is important for understanding 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

The Hidden Secret of the 4% Rule

The "hidden secret" of the 4% Rule isn't so much a secret as it is a crucial understanding: it's aguideline, not a rigid law. The true power lies in its adaptability. The initial 4% withdrawal is just the starting point. The key to long-term success is to actively manage your spending and adjust your withdrawal rate based on market performance and your personal circumstances. For example, if your portfolio performs exceptionally well in a given year, you might consider taking a slightly larger withdrawal, knowing that your nest egg has grown. Conversely, if the market takes a significant downturn, you might need to tighten your belt and reduce your withdrawals to protect your capital. Another aspect often overlooked is the importance of diversification. While Bengen's initial research focused on a 50/50 stock/bond portfolio, your optimal asset allocation may be different depending on your risk tolerance and time horizon. Consulting with a financial advisor can help you create a personalized investment strategy that aligns with your retirement goals. Ultimately, the 4% Rule is a powerful tool for financial planning, but it requires ongoing monitoring, adjustments, and a deep understanding of your own financial situation. Diversification is another aspect that is often overlooked, understanding your own financial situation and risk tolerance. The key to long-term success is to actively manage your spending and adjust your withdrawal rate based on market performance and your personal circumstances for 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

Recommendations for Using the 4% Rule

If you're considering using the 4% Rule for your retirement planning, here are some recommendations to keep in mind. First, don't treat it as gospel. It's a helpful starting point, but it's not a foolproof formula. Be prepared to adjust your withdrawal rate as needed based on market conditions and your personal circumstances. Second, factor in all your potential income sources. This includes Social Security, pensions, and any other sources of revenue you might have. These additional income streams can reduce your reliance on your investment portfolio and potentially allow for a higher withdrawal rate. Third, consider your life expectancy. The 4% Rule is typically based on a 30-year retirement period. If you expect to live longer, you may need to lower your withdrawal rate to ensure your savings last. Fourth, be realistic about your spending habits. Track your expenses carefully and create a detailed budget for your retirement years. This will help you accurately estimate your income needs and determine a sustainable withdrawal rate. Finally, don't be afraid to seek professional advice. A qualified financial advisor can help you develop a personalized retirement plan that takes into account your unique circumstances and goals. A financial advisor can also help to create a personalized investment strategy that aligns with your retirement goals, which is related to 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025). The 4% Rule is typically based on a 30-year retirement period, so you may need to lower your withdrawal rate to ensure your savings last longer.

Understanding Inflation and its Impact

Inflation is a critical factor to consider when using the 4% Rule. The rule assumes that you'll adjust your withdrawals each year to account for inflation, ensuring that your purchasing power remains constant. However, accurately predicting future inflation rates is notoriously difficult. High inflation can erode the value of your savings more quickly than anticipated, potentially jeopardizing your retirement plan. To mitigate this risk, consider using a conservative inflation assumption when calculating your initial withdrawal amount. You can also explore strategies for hedging against inflation, such as investing in Treasury Inflation-Protected Securities (TIPS). These securities are designed to protect investors from inflation by adjusting their principal value based on changes in the Consumer Price Index (CPI). Another important consideration is that inflation doesn't affect all goods and services equally. Healthcare costs, for example, tend to rise faster than the average inflation rate. If you anticipate significant healthcare expenses in retirement, you may need to factor this into your withdrawal plan. By carefully considering the potential impact of inflation and taking steps to protect your savings, you can increase the likelihood of a successful retirement. Investing in Treasury Inflation-Protected Securities (TIPS) is a strategy for hedging against inflation and protecting the investors. Accurately predicting future inflation rates is notoriously difficult, as well as how it will impact 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

Tips for Maximizing the 4% Rule

Want to make the 4% Rule work even harder for you? Here are a few tips to consider: Embrace frugality: The less you spend, the longer your savings will last. Identify areas where you can cut back on expenses without sacrificing your quality of life. Consider a side hustle: Even a small amount of extra income can significantly reduce your reliance on your retirement savings. Explore opportunities to generate passive income or pursue a part-time job that you enjoy. Optimize your asset allocation: Regularly review your investment portfolio and make adjustments as needed to ensure it aligns with your risk tolerance and retirement goals. Consider delaying retirement: Even a few extra years of working can make a big difference in the size of your nest egg and the sustainability of your withdrawals. Be flexible: The 4% Rule is not a rigid formula. Be prepared to adjust your spending and withdrawal rate as needed based on market conditions and your personal circumstances. By implementing these tips, you can increase your chances of a successful and fulfilling retirement. Delaying retirement can make a big difference in the size of your nest egg and the sustainability of your withdrawals. Those are some tips for maximizing 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

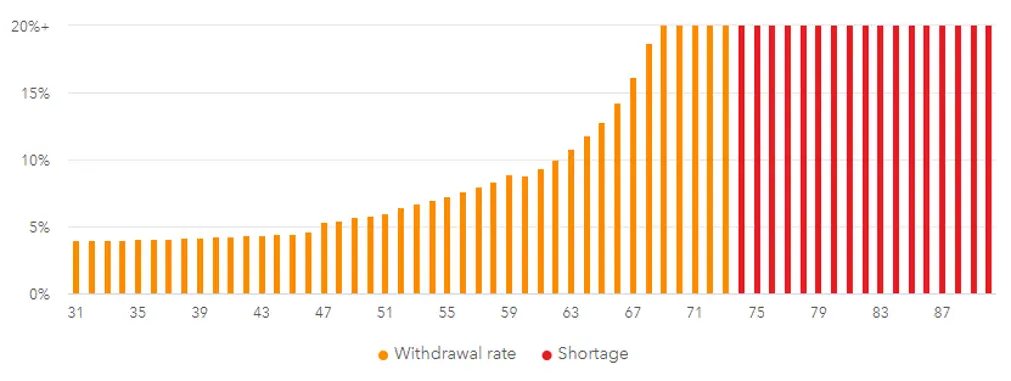

Understanding Sequence of Returns Risk

Sequence of returns risk refers to the danger of experiencing negative investment returns early in your retirement. If your portfolio takes a significant hit in the first few years of withdrawals, it can severely deplete your capital and make it much harder to recover. This is because you're not only losing money on your investments, but you're also withdrawing funds to cover your living expenses. To mitigate sequence of returns risk, consider the following strategies: Maintain a diversified portfolio: Don't put all your eggs in one basket. Diversify your investments across different asset classes to reduce your overall risk. Use a "bucket" strategy: Divide your retirement savings into different buckets based on your time horizon. For example, you might have a "short-term" bucket for immediate expenses, a "mid-term" bucket for expenses in the next 5-10 years, and a "long-term" bucket for growth investments. Consider a variable withdrawal strategy: Instead of withdrawing a fixed percentage each year, adjust your withdrawals based on market performance. In years with strong returns, you can withdraw more, and in years with poor returns, you can withdraw less. Work with a financial advisor: A qualified advisor can help you develop a personalized investment strategy that takes into account your risk tolerance and retirement goals. Understanding sequence of returns risk is crucial for protecting your retirement savings from market volatility. Sequence of returns risk refers to the danger of experiencing negative investment returns early in your retirement which could severly deplete your capital. Maintaining a diversified portfolio is an important strategy to consider when learning about 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

Fun Facts About the 4% Rule

Did you know that the 4% Rule has sparked heated debates among financial experts? Some argue that it's too conservative, while others believe it's too risky. This ongoing debate highlights the importance of understanding the rule's limitations and tailoring it to your individual circumstances. Another fun fact: the 4% Rule was originally based on historical data from the United States. While it can be applied to other countries, it's important to consider differences in market conditions, inflation rates, and tax laws. The 4% Rule has inspired countless individuals to pursue financial independence and early retirement. It has become a cornerstone of the FIRE (Financial Independence, Retire Early) movement, empowering people to take control of their finances and design a life on their own terms. Despite its popularity, the 4% Rule is not a get-rich-quick scheme. It requires discipline, planning, and a willingness to adapt to changing circumstances. But for those who are committed to financial freedom, it can be a powerful tool for achieving their dreams. The 4% Rule has inspired countless individuals to pursue financial independence and early retirement, helping people to take control of their finances. Financial independence is an important term related to 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

How to Calculate Your 4% Rule Number

Calculating your 4% Rule number is a straightforward process. First, estimate your annual retirement expenses. This includes everything from housing and food to healthcare and entertainment. Be sure to factor in inflation and any unexpected expenses that might arise. Next, determine your potential income sources. This includes Social Security, pensions, and any other sources of revenue you might have. Subtract your income from your expenses to determine the amount you'll need to withdraw from your investment portfolio each year. Finally, divide your annual withdrawal amount by 0.04 (4%) to calculate the size of the nest egg you'll need to support your retirement. For example, if you estimate that you'll need to withdraw $40,000 per year from your portfolio, you'll need a nest egg of $1 million ($40,000 /

0.04 = $1,000,000). It's important to remember that this is just an estimate. You may need to adjust your withdrawal rate based on market conditions and your personal circumstances. Consulting with a financial advisor can help you develop a more accurate and personalized retirement plan. It's important to factor in inflation and any unexpected expenses that might arise in your retirement years when calculating 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025). It has become a cornerstone of the FIRE (Financial Independence, Retire Early) movement, empowering people to take control of their finances and design a life on their own terms.

What If the 4% Rule Fails?

Let's face it, even the best-laid plans can go awry. What happens if the 4% Rule fails, and you find yourself running out of money in retirement? Don't panic! There are several steps you can take to mitigate the damage. First, cut back on your spending. Identify areas where you can reduce your expenses without sacrificing your quality of life. Even small changes can make a big difference over time. Second, consider generating additional income. Explore opportunities to pursue a part-time job, start a side hustle, or rent out a spare room. Third, re-evaluate your investment portfolio. Consider shifting to a more conservative asset allocation to reduce your risk. Fourth, explore options for delaying Social Security benefits. The longer you wait to claim Social Security, the higher your monthly payments will be. Finally, seek professional advice. A qualified financial advisor can help you develop a plan to get back on track and ensure your long-term financial security. Remember, running out of money in retirement is not the end of the world. With careful planning and a willingness to adapt, you can overcome this challenge and still enjoy a fulfilling retirement. Consider shifting to a more conservative asset allocation to reduce your risk. Generating additional income and reducing your expenses can help you get back on track with 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

Listicle: 5 Ways to Supercharge Your 4% Rule Strategy

Ready to take your 4% Rule strategy to the next level? Here are five actionable tips: 1. Embrace Tax-Advantaged Accounts: Maximize your contributions to 401(k)s, IRAs, and other tax-advantaged accounts to reduce your tax burden and grow your savings faster.

2. Consider Geolocation Arbitrage: Explore opportunities to live in a lower-cost area, either domestically or internationally, to reduce your expenses and extend your retirement savings.

3. Optimize Your Healthcare Costs: Shop around for the best health insurance rates, take advantage of preventative care services, and consider health savings accounts (HSAs) to manage your healthcare expenses.

4. Invest in Dividend-Paying Stocks: Generate a steady stream of passive income from dividend-paying stocks to supplement your withdrawals and reduce your reliance on selling your investments.

5. Continuously Educate Yourself: Stay informed about market trends, financial planning strategies, and tax laws to make informed decisions and optimize your retirement plan. By implementing these strategies, you can supercharge your 4% Rule strategy and increase your chances of a successful and fulfilling retirement. Stay informed about market trends, financial planning strategies, and tax laws to make informed decisions and optimize your retirement plan. It is important to consider geolocation arbitrage when wanting to optimize your retirement savings with 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025).

Question and Answer

Q: Is the 4% Rule still relevant in 2025?

A: Yes, the 4% Rule remains a valuable starting point for retirement planning, but it's crucial to adapt it to your individual circumstances and market conditions. Consider factors like life expectancy, risk tolerance, and current interest rates.

Q: What are the biggest risks to the 4% Rule?

A: The biggest risks include high inflation, unexpected market downturns, and underestimating your retirement expenses. Be prepared to adjust your spending and withdrawal rate as needed to mitigate these risks.

Q: Can I withdraw more than 4% if my portfolio performs well?

A: Yes, you can consider withdrawing more than 4% in years with strong portfolio performance, but be cautious and avoid overspending. It's important to maintain a buffer to protect against future market downturns.

Q: Where can I find a reliable 4% Rule calculator?

A: There are many online 4% Rule calculators available, but be sure to use one from a reputable source. You can also consult with a financial advisor to develop a personalized retirement plan.

Conclusion of 4% Rule Calculator: Safe Withdrawal Rate for Early Retirement (Updated 2025)

The 4% Rule, updated for 2025, provides a valuable framework for planning a sustainable early retirement. While not a foolproof guarantee, it serves as a useful starting point for estimating a safe withdrawal rate. Remember to personalize the rule based on your unique circumstances, considering factors such as risk tolerance, life expectancy, and potential income sources. Stay informed, be flexible, and don't hesitate to seek professional advice. By taking a proactive approach to your retirement planning, you can increase your chances of achieving financial freedom and enjoying a fulfilling retirement.

Post a Comment