Coast FIRE Calculator: How Much Money You Need to Never Save Again (2025)

Imagine a life where you no longerhaveto save for retirement. Sounds too good to be true, right? What if I told you there's a way to reach a point where your existing investments are projected to grow enough to cover your retirement, allowing you to focus on other financial goals or simply enjoy life more? That's where Coast FIRE comes in, and understanding how to calculate your Coast FIRE number is the first step toward this liberating possibility.

The traditional path to retirement can feel daunting. Decades of diligent saving, constant monitoring of investment performance, and the ever-present worry of outliving your money can lead to stress and a feeling of being trapped in a cycle of work and save. Many people find themselves questioning if they're saving enough, if their investments are on track, and if they'll ever truly be able to step away from full-time work.

This blog post will guide you through understanding Coast FIRE, explaining what it is, how to calculate it using a Coast FIRE calculator, and ultimately, how much money you need to reach the point where you can potentially stop actively saving for retirement. We'll explore the factors that influence your Coast FIRE number, the assumptions involved, and how you can use this information to make informed financial decisions and design a lifestyle that aligns with your values.

This article explores the concept of Coast FIRE, a financial milestone where your existing investments are projected to grow enough to cover your retirement needs, allowing you to potentially stop actively saving. We'll delve into the use of Coast FIRE calculators, the key factors influencing your target number, and the underlying principles of compound interest and time value of money. Understanding Coast FIRE can empower you to make informed financial choices and design a lifestyle that prioritizes freedom and flexibility. It is related to financial independence, retirement planning, investing, early retirement, and personal finance.

My Journey to Coast FIRE Awareness

My first encounter with the term "Coast FIRE" was almost accidental. I was deep-diving into the FIRE (Financial Independence, Retire Early) movement, feeling both inspired and slightly overwhelmed by the sheer scale of savings required for full financial independence. It felt like climbing a mountain with no peak in sight. Then, I stumbled upon a blog post that mentioned Coast FIRE, and a lightbulb went off. The idea of reaching a point where I could essentially "set and forget" my retirement savings, allowing them to grow on their own, was incredibly appealing.

I remember the initial feeling of skepticism. Could it really be that simple? Was it just another internet pipe dream? But the more I researched, the more I realized the power of compounding and the potential of early investing. It wasn't about magic; it was about math.

My own journey involved a lot of spreadsheet tinkering and online calculator use. I played with different scenarios, adjusting my projected retirement age, estimated expenses, and investment returns. The results were eye-opening. I realized I was already further along than I thought, and that reaching Coast FIRE was a tangible goal within reach. This realization freed me up to focus on other aspects of my life, like pursuing passion projects and spending more time with family, without the constant pressure of needing to aggressively save every penny. Coast FIRE provides a sense of security and the option to deaccelerate and enjoy life at a more relaxed pace.

What Exactly is Coast FIRE?

Coast FIRE is a financial independence strategy that focuses on reaching a point where you no longer need to actively save for retirement. Instead, your existing investments are projected to grow sufficiently over time to cover your retirement expenses. Think of it as setting your retirement plan in motion and then "coasting" to the finish line. You still need to work and cover your current living expenses, but you're no longer contributing to your retirement accounts.

Unlike full FIRE, which aims for complete financial independence and the ability to retire early without any earned income, Coast FIRE offers more flexibility. It allows you to downshift to a less demanding or higher-purpose career, start a business, or pursue other interests, knowing that your retirement is essentially taken care of. It's a great option for those who enjoy working but want more control over their time and energy.

The beauty of Coast FIRE lies in the power of compound interest. By investing early and allowing your money to grow over a longer period, you can significantly reduce the amount you need to actively save. Time is your greatest ally in this strategy. The earlier you start investing, the less you need to save each year to reach your Coast FIRE number. It's about leveraging the magic of compounding to create a secure financial future without the constant pressure of aggressive saving.

The History and Myth of Coast FIRE

The concept of Coast FIRE, while relatively new in name, has roots in the principles of long-term investing and the power of compound interest, ideas that have been around for centuries. The formalization of the term "Coast FIRE" is more recent, likely emerging alongside the broader FIRE movement as people sought more nuanced approaches to financial independence.

One of the biggest myths surrounding Coast FIRE is that it's easy. While it's true that you eventually stopactivelysaving for retirement, reaching your Coast FIRE number still requires significant effort and discipline. It often involves years of diligent saving, strategic investing, and careful budgeting. It's not a get-rich-quick scheme; it's a long-term strategy that requires commitment and planning.

Another myth is that Coast FIRE is only for young people. While starting early certainly has its advantages, Coast FIRE is achievable at any age. It simply requires a different approach and potentially more aggressive saving in the initial years. Regardless of your age, calculating your Coast FIRE number can provide valuable insights into your financial situation and help you make informed decisions about your future. Understanding the truth behind Coast FIRE, separating fact from fiction, is crucial for making it a viable and sustainable strategy.

The Hidden Secrets of the Coast FIRE Calculator

While Coast FIRE calculators appear straightforward, they conceal subtle assumptions and factors that can significantly impact the results. One of the most critical, and often overlooked, elements is the projected rate of return on your investments. Calculators typically use a standard percentage, but the actual returns can fluctuate greatly depending on your investment strategy, market conditions, and risk tolerance. A seemingly small difference in the projected rate of return can have a huge impact on your Coast FIRE number and the time it takes to reach it.

Another hidden secret lies in accurately estimating your future retirement expenses. Many people underestimate how much they'll need to cover healthcare costs, travel, and other discretionary spending. It's essential to factor in inflation and potential lifestyle changes when projecting your expenses. Underestimating your expenses can lead to a rude awakening later in life.

Furthermore, Coast FIRE calculators often don't account for unexpected life events, such as job loss, medical emergencies, or major home repairs. It's prudent to have a buffer in your calculations to account for these unforeseen circumstances. Don't rely solely on the calculator's output; use it as a starting point and adjust the variables based on your individual circumstances and risk tolerance. Understanding these hidden secrets can help you create a more realistic and robust Coast FIRE plan.

Recommendation of Coast FIRE Calculator

Choosing the right Coast FIRE calculator is crucial for accurate planning. There are many free online calculators available, but it's important to select one that is comprehensive, user-friendly, and allows you to customize the key variables. Look for calculators that allow you to adjust your projected retirement age, estimated expenses, investment returns, and inflation rate.

Beyond simply using a calculator, it's highly recommended to consult with a financial advisor. A qualified advisor can provide personalized guidance, help you develop a tailored investment strategy, and assess your risk tolerance. They can also help you navigate complex financial situations, such as tax implications and estate planning.

Another recommendation is to regularly review and update your Coast FIRE plan. Life circumstances change, and your financial goals may evolve over time. It's important to reassess your progress and make adjustments as needed. This might involve increasing your savings rate, adjusting your investment strategy, or delaying your retirement date. The key is to stay flexible and adaptable to changing conditions. Don't set it and forget it; regularly monitor and adjust your plan to ensure you stay on track toward your Coast FIRE goals.

Understanding the Underlying Assumptions

Coast FIRE calculators rely on several key assumptions that can significantly impact the accuracy of their results. Understanding these assumptions is crucial for interpreting the results and making informed financial decisions. One of the most important assumptions is the projected rate of return on your investments. This is essentially an educated guess about how much your investments will grow over time. Calculators typically use a historical average, but past performance is not necessarily indicative of future results. Market conditions can change, and your investment returns may vary significantly from year to year.

Another key assumption is the inflation rate. Inflation erodes the purchasing power of your money over time, so it's important to factor it into your calculations. Calculators typically use a historical average inflation rate, but the actual inflation rate can fluctuate depending on economic conditions. Underestimating the inflation rate can lead to underestimating your future retirement expenses.

Furthermore, Coast FIRE calculators often assume a consistent savings rate and investment strategy. In reality, your savings rate may vary depending on your income, expenses, and financial goals. You may also need to adjust your investment strategy over time to account for changes in your risk tolerance and market conditions. Understanding these underlying assumptions and their potential impact can help you create a more realistic and robust Coast FIRE plan.

Tips for Using a Coast FIRE Calculator Effectively

Using a Coast FIRE calculator effectively involves more than just plugging in numbers. Here are some tips to help you get the most out of this tool: Be realistic with your assumptions. Don't overestimate your investment returns or underestimate your future expenses. Use conservative estimates to account for potential market fluctuations and unexpected life events. Play with different scenarios. Experiment with different retirement ages, expense levels, and investment returns to see how they impact your Coast FIRE number. This can help you understand the trade-offs and make informed decisions.

Factor in taxes. Remember that investment returns are subject to taxes, which can significantly reduce your net returns. Be sure to factor in taxes when estimating your future retirement income. Consider healthcare costs. Healthcare costs are a major expense in retirement, so it's important to factor them into your calculations. Research the cost of healthcare in your area and estimate your future healthcare expenses. Don't forget about inflation. Inflation erodes the purchasing power of your money over time, so it's important to factor it into your calculations. Use a realistic inflation rate to estimate your future expenses. Regularly review and update your plan. Your life circumstances and financial goals may change over time, so it's important to review and update your Coast FIRE plan regularly. Make adjustments as needed to stay on track toward your goals. Using these tips can help you use a Coast FIRE calculator more effectively and create a more realistic and robust financial plan.

How to Adjust for Inflation

Inflation is a silent thief, slowly eroding the value of your savings over time. When planning for Coast FIRE, it's absolutely crucial to account for inflation to ensure your projected retirement income will actually cover your expenses. A common mistake is to calculate your Coast FIRE number based on today's expenses without considering how much those expenses will increase in the future.

There are a couple of ways to adjust for inflation when using a Coast FIRE calculator. One approach is to use a real rate of return, which is the nominal rate of return minus the inflation rate. This gives you a more accurate picture of the actual growth of your investments after accounting for inflation. For example, if your investments are expected to return 8% per year and the inflation rate is 3%, your real rate of return is 5%.

Another approach is to estimate your future expenses in today's dollars and then inflate them to your projected retirement year. This involves using an assumed inflation rate to project how much your expenses will increase over time. For example, if you estimate that you'll need $50,000 per year in today's dollars to cover your retirement expenses and the inflation rate is 3%, you'll need approximately $121,000 per year in 40 years to maintain the same standard of living. Adjusting for inflation is essential for creating a realistic and sustainable Coast FIRE plan.

Fun Facts About Coast FIRE

Did you know that reaching Coast FIRE can potentially free up a significant portion of your income? Once you reach Coast FIRE, you no longer need to actively save for retirement, which means you can redirect those savings to other goals, such as paying off debt, traveling, or pursuing passion projects. Coast FIRE can also provide a greater sense of financial security and peace of mind. Knowing that your retirement is essentially taken care of can reduce stress and allow you to focus on other aspects of your life.

Another fun fact is that Coast FIRE can be a stepping stone to full financial independence. While Coast FIRE doesn't necessarily mean you can retire early without any earned income, it can significantly reduce the amount you need to save to reach full FIRE. This can make full FIRE more attainable and accelerate your path to financial freedom. Coast FIRE offers flexibility in career choices. It allows you to choose a job that you truly enjoy, even if it pays less, knowing that your retirement is already secured. This can lead to a more fulfilling and meaningful career. Coast FIRE offers a unique blend of financial security and flexibility, making it an attractive option for many people.

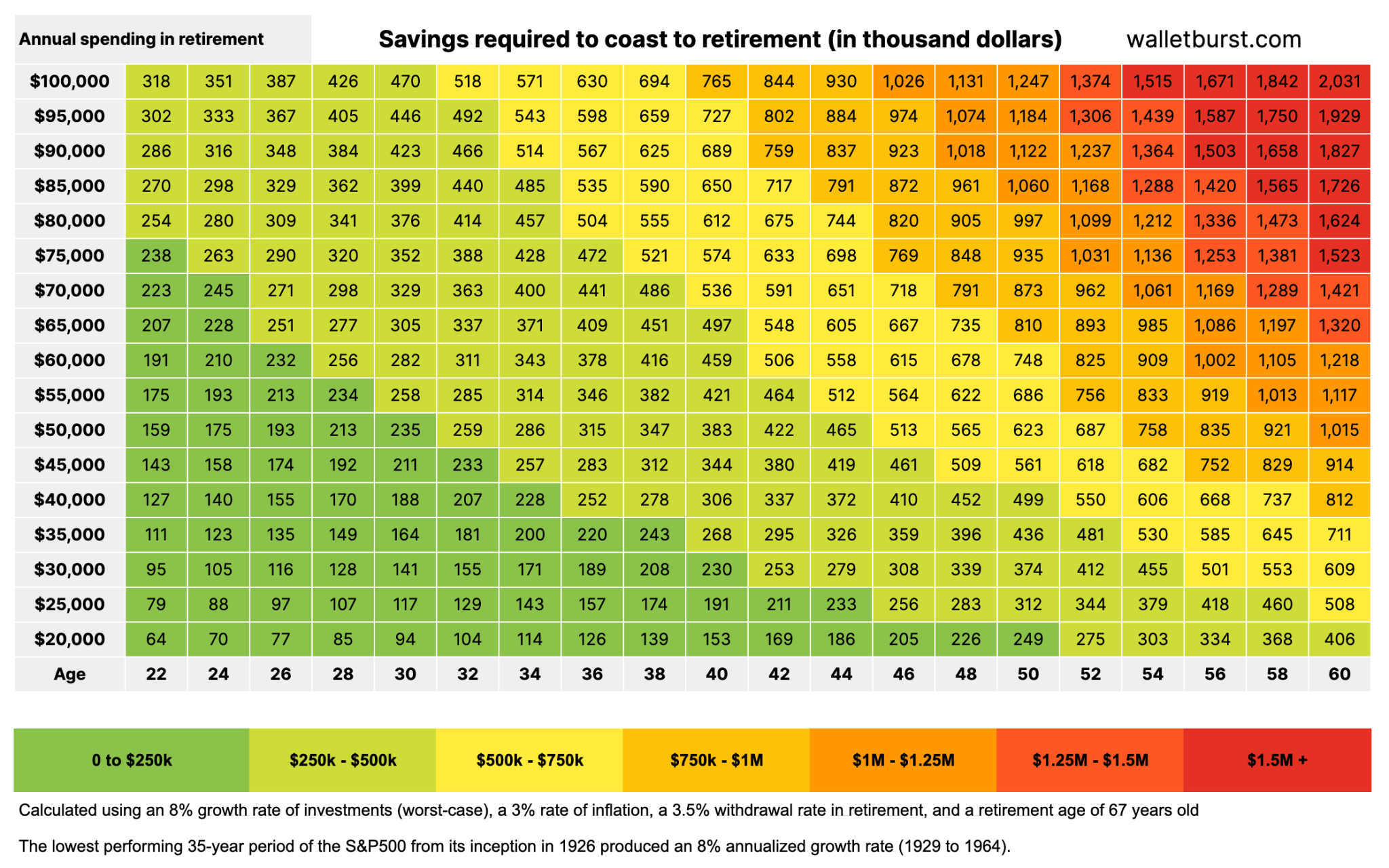

How to Calculate Your Coast FIRE Number

Calculating your Coast FIRE number involves a few key steps. First, you need to estimate your annual retirement expenses. This includes all the expenses you expect to incur in retirement, such as housing, food, transportation, healthcare, and entertainment. Be sure to factor in inflation and potential lifestyle changes. Next, you need to determine your projected retirement age. This is the age at which you plan to stop actively saving for retirement. Consider your health, career goals, and financial situation when making this decision.

Then, you need to estimate your investment returns. This is the rate of return you expect to earn on your investments over the long term. Use a conservative estimate to account for potential market fluctuations. Now you need to use a Coast FIRE calculator to determine how much money you need to have invested at your projected retirement age to cover your retirement expenses. There are many free online calculators available, or you can consult with a financial advisor. Finally, once you have your Coast FIRE number, you can track your progress and make adjustments as needed to stay on track toward your goals. Calculating your Coast FIRE number is a crucial step in designing a financial plan that aligns with your values and goals.

What If You Miss Your Coast FIRE Target?

Life happens, and sometimes things don't go according to plan. What if you fall short of your Coast FIRE target? Don't panic! There are several steps you can take to get back on track. First, reassess your expenses. Look for ways to reduce your spending and increase your savings rate. Even small changes can make a big difference over time. Consider delaying your retirement date. Working for a few extra years can significantly increase your savings and reduce the amount you need to withdraw from your investments each year.

Adjust your investment strategy. Consider increasing your risk tolerance or diversifying your portfolio to potentially earn higher returns. Consult with a financial advisor to get personalized recommendations. Seek additional income streams. Look for opportunities to earn extra money through side hustles, part-time jobs, or freelance work. Every little bit helps. Remember that Coast FIRE is a journey, not a destination. It's okay to adjust your plan as needed to adapt to changing circumstances. The key is to stay flexible, proactive, and committed to your financial goals. Missing your Coast FIRE target is not the end of the world; it's an opportunity to re-evaluate your plan and make adjustments to get back on track.

Top 5 Listicle of Coast FIRE Tips and Tricks

Here are 5 top tips and tricks to help you achieve Coast FIRE: Start early and invest consistently. The earlier you start investing, the less you need to save each year to reach your Coast FIRE number. Make it a habit to invest a portion of your income regularly. Automate your savings. Set up automatic transfers from your checking account to your investment accounts to ensure you're consistently saving. This can help you avoid the temptation to spend your money.

Minimize your expenses. Reducing your expenses can free up more money to save and invest. Look for ways to cut back on unnecessary spending and live a more frugal lifestyle. Increase your income. Finding ways to earn extra money can accelerate your path to Coast FIRE. Consider side hustles, part-time jobs, or freelance work. Stay informed and educated. The more you know about personal finance and investing, the better equipped you'll be to make informed decisions and achieve your Coast FIRE goals. These tips and tricks can help you stay motivated, focused, and on track toward your Coast FIRE goals.

Question and Answer

Here are some frequently asked questions about Coast FIRE:

Question: How is Coast FIRE different from traditional retirement planning?

Answer: Traditional retirement planning focuses on saving a specific amount of money by retirement, while Coast FIRE focuses on having enough invested early enough that it will grow to the needed retirement amount, without further contributions.

Question: Is Coast FIRE risky?

Answer: Coast FIRE, like any financial strategy, has risks. Market downturns can impact investment growth, and unexpected expenses can derail plans. A conservative approach and regular monitoring are crucial.

Question: Can I achieve Coast FIRE if I'm starting later in life?

Answer: Yes, but it may require more aggressive saving initially. A financial advisor can help create a tailored plan to catch up and leverage the power of compounding.

Question: What if my expenses change significantly after reaching Coast FIRE?

Answer: Flexibility is key. Reassess your budget regularly and be prepared to adjust your spending or temporarily resume saving if needed. Coast FIRE is a guideline, not a rigid rule.

Conclusion of Coast FIRE Calculator: How Much Money You Need to Never Save Again (2025)

Coast FIRE represents a compelling alternative to the traditional, often stressful, path to retirement. By understanding the principles behind it and utilizing a Coast FIRE calculator effectively, you can gain valuable insights into your financial trajectory and potentially unlock a future where you have more control over your time and energy. Remember to be realistic with your assumptions, regularly review your plan, and seek professional advice when needed. Coast FIRE isn't about escaping work entirely; it's about creating a life where your work aligns with your values and your financial future is secure, allowing you to "coast" towards a fulfilling retirement.

Post a Comment